When buying life insurance, the focus often falls on the type of cover or the sum assured. However, one crucial aspect that’s sometimes overlooked is how you’ll pay for it. The premium payment structure can significantly influence the policy’s affordability and long-term value.

Understanding the options available can help you make a smarter financial choice that aligns with your income flow, goals, and stage in life. This article breaks down the two primary payment methods: single and regular premiums, helping you decide which plan suits you best.

What is a Single Premium Term Life Insurance Plan?

A single premium term insurance plan requires a one-time lump sum payment at the time of purchase. This upfront payment covers the entire policy duration, ensuring you won’t have to worry about future premium dues.

It is often chosen by individuals with surplus funds who want lifelong coverage or investment benefits without the hassle of recurring payments. Depending on the plan's structure, the policy remains in force for the full term or until the insured’s death.

What is a Regular Premium Term Life Insurance Plan?

A regular premium life insurance plan allows you to pay premiums periodically- monthly, quarterly, half-yearly, or annually- throughout the policy term or for a fixed number of years. This makes it easier for policyholders to manage payments as part of their regular financial planning.

Regular premium plans are suitable for individuals with a steady income who prefer spreading the cost of insurance over time rather than paying a large sum upfront. These plans often offer flexibility regarding premium payment frequency and policy duration.

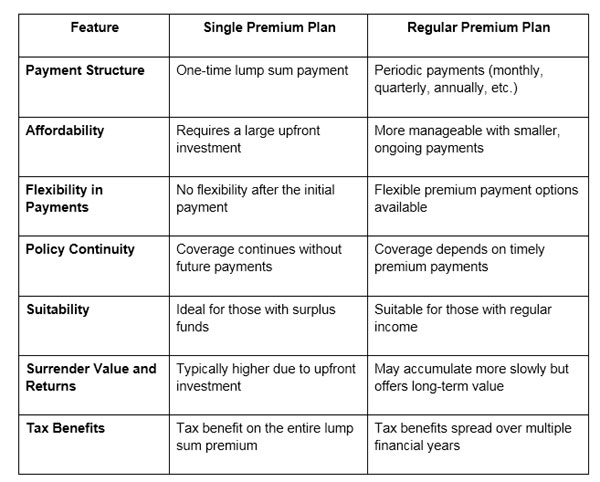

Key Differences Between Single and Regular Premium Plans

While single and regular premium plans aim to provide life insurance coverage, they differ significantly in how premiums are paid and the policy's functions. Here’s a quick comparison to help you understand the distinctions:

Pros and Cons of Single Premium Plans

Single-premium life insurance plans offer simplicity and immediate coverage, but they may not be suitable for everyone. Here’s a look at their key advantages and disadvantages:

Advantages of Single Premium Plans

- One-Time Payment: You pay the premium just once, making it hassle-free and ideal for those who want to avoid ongoing financial commitments.

- Immediate Coverage: Coverage starts as soon as the lump sum is paid, offering quick protection.

- Higher Returns: These plans often generate better maturity or surrender values due to the upfront investment.

- Tax Efficiency: You can claim a tax deduction on the entire premium amount in the same financial year under Section 80C of the Income Tax Act.

Disadvantages of Single Premium Plans

- High Initial Cost: Requires a significant lump sum, which may not be feasible for many individuals.

- Limited Flexibility: No option to adjust or pause premium payments once made.

- Opportunity Cost: Investing a large sum upfront may limit your ability to invest in other financial avenues.

Pros and Cons of Regular Premium Plans

Regular premium life insurance plans allow for systematic payments over time, making them a practical choice for many policyholders. Here's a look at their benefits and limitations:

Advantages of Regular Premium Plans

- Affordable Payments: Premiums are spread across monthly, quarterly, or annual intervals, making it easier to manage within a budget.

- Flexible Duration: You can select the premium payment term that best suits your financial goals and earning capacity.

- Encourages Financial Discipline: Regular payments promote saving habits and long-term financial planning.

- Better Customisation: These plans often come with the option to add riders or increase coverage during the policy term.

Disadvantages of Regular Premium Plans

- Long-Term Commitment: Missing or delaying payments could lead to policy lapse or reduced benefits.

- Higher Total Cost: Over time, the cumulative premium paid may be more than a single premium plan for the same coverage.

- Inflation Impact: Fixed premium amounts may feel more burdensome as living costs rise.

Single vs Regular Premiums: Which Plan Should You Choose?

Depending on your financial situation, lifestyle, and long-term goals, you can choose between single and regular premium term life insurance plans.

Who Should Choose Single Premium Plans?

If you have a lump sum amount available, like from a bonus, inheritance, or matured investment, a single premium plan may be suitable. It ensures lifetime coverage with one payment and avoids the hassle of ongoing premiums.

It’s also a preferred option for those who want a paid-up policy without future financial commitments.

Who Should Choose Regular Premium Plans?

A regular premium plan offers greater flexibility if you have a regular income and prefer budgeting your expenses over time. It lets you maintain liquidity while gradually building long-term coverage.

It's also better suited for individuals who value ongoing engagement with their policy and may want to make adjustments over time.

When exploring life insurance options, there are a range of plans available with flexible premium structures designed to fit different financial needs and lifestyles. Choosing the right premium payment plan is just as important as selecting the right coverage.

Whether you opt for a single premium or regular premium plan, the decision should align with your current financial standing, future income stability, and preference. By weighing your goals and financial capacity, you can select a plan that fits seamlessly into your financial strategy.